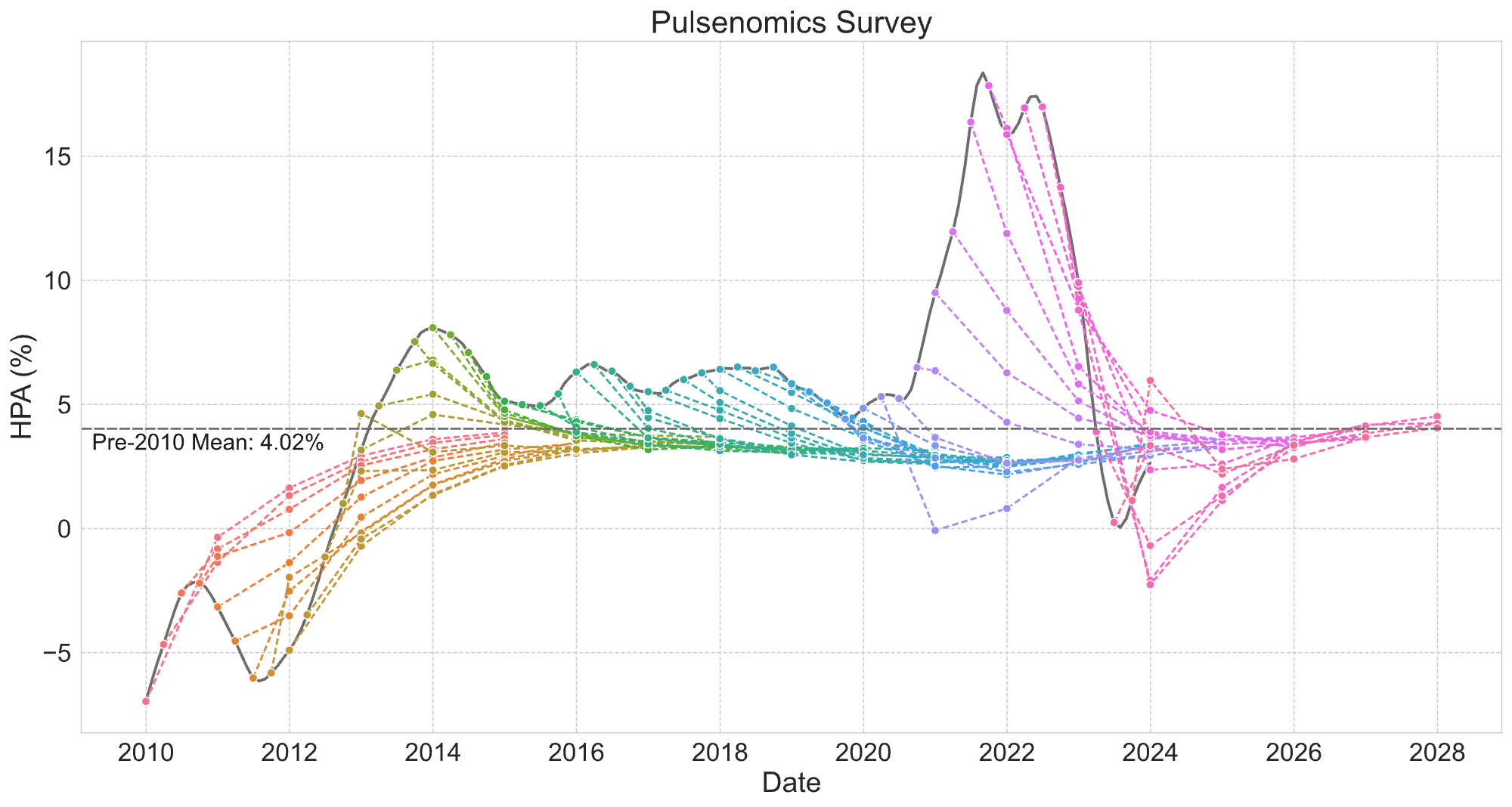

Seemingly puzzling patterns in house price growth forecasts are largely consistent with a model in which forecasters are uncertain about future long-run house price growth and have different prior beliefs. We employ large-scale cloud computing and a state-of-the-art learning model to demonstrate this effect based on a novel dataset.

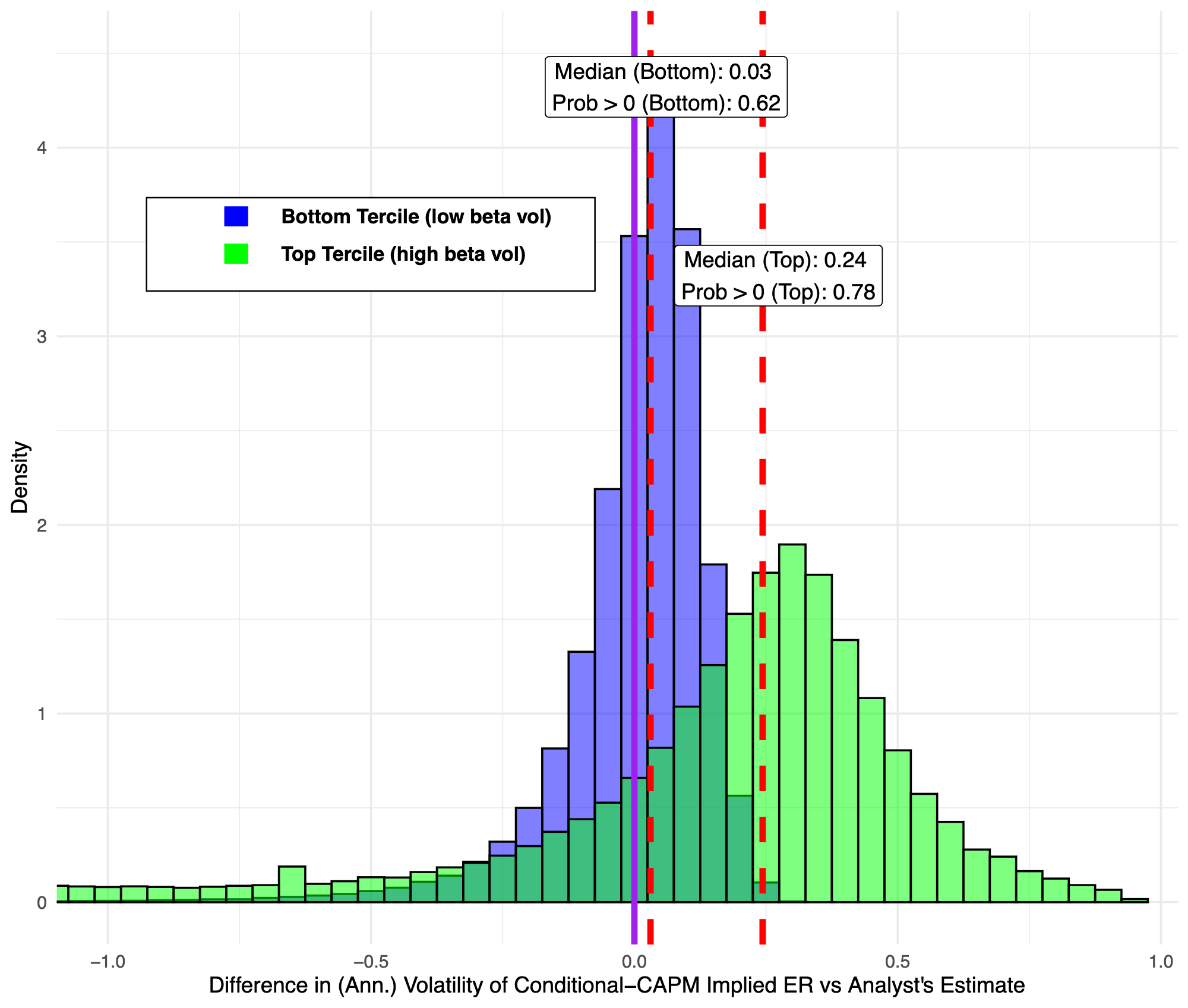

Investors underestimate the volatility of discount rates, which leads to asset pricing anomalies. A measure based on this underestimation explains 12 prominent cross-sectional anomalies.

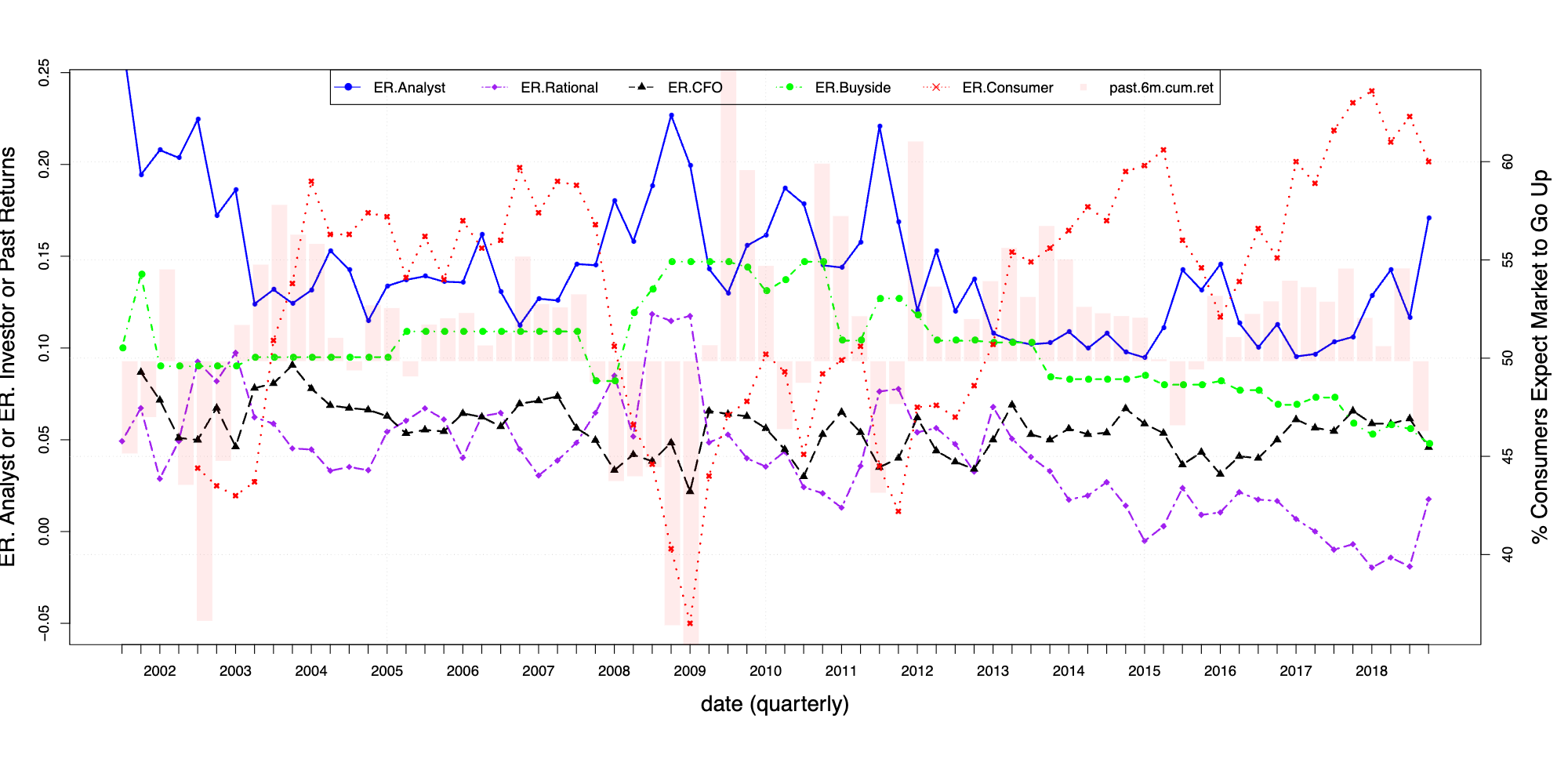

Wall Street and Main Street expectations about future stock returns are persistently opposed to each other. I demonstrate that this disagreement persists when they hold divergent views regarding how fundamental news relates to future stock prices.

Uncertainty variations lead to opposite relationships with market efficiency over-time vs. cross-firm. We build an information-choice model to demonstrate this theoretically and confirm it empirically using analysts' forecast biases.

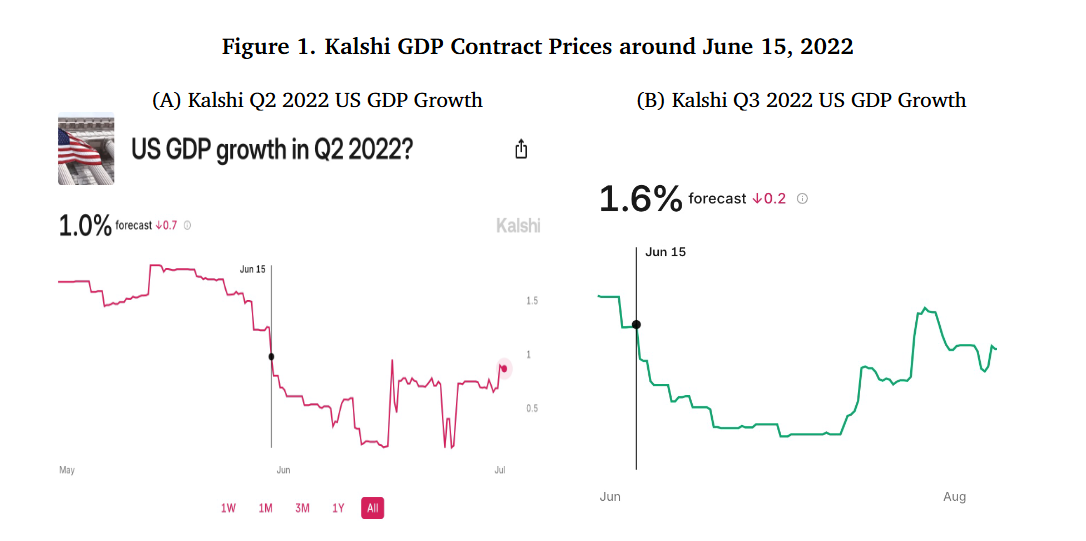

Traders in the Kalshi event contract markets are believers in the standard monetary policy transmission channels rather than the ‘Fed Information Effects.’ We use novel high-frequency data to identify this effect.